Advanced Risk Management Tools with MSTAR

Our products are built on over 15 years of applied research in operational risk.

MSTAR Desktop is our core tool for designing and simulating risk scenarios.

MSTAR Platform includes a curated news feed and a library of operational risk scenarios, and can be fully customised for internal deployment.

These tools are trusted by leading financial institutions for scenario-based risk analysis and regulatory use cases.

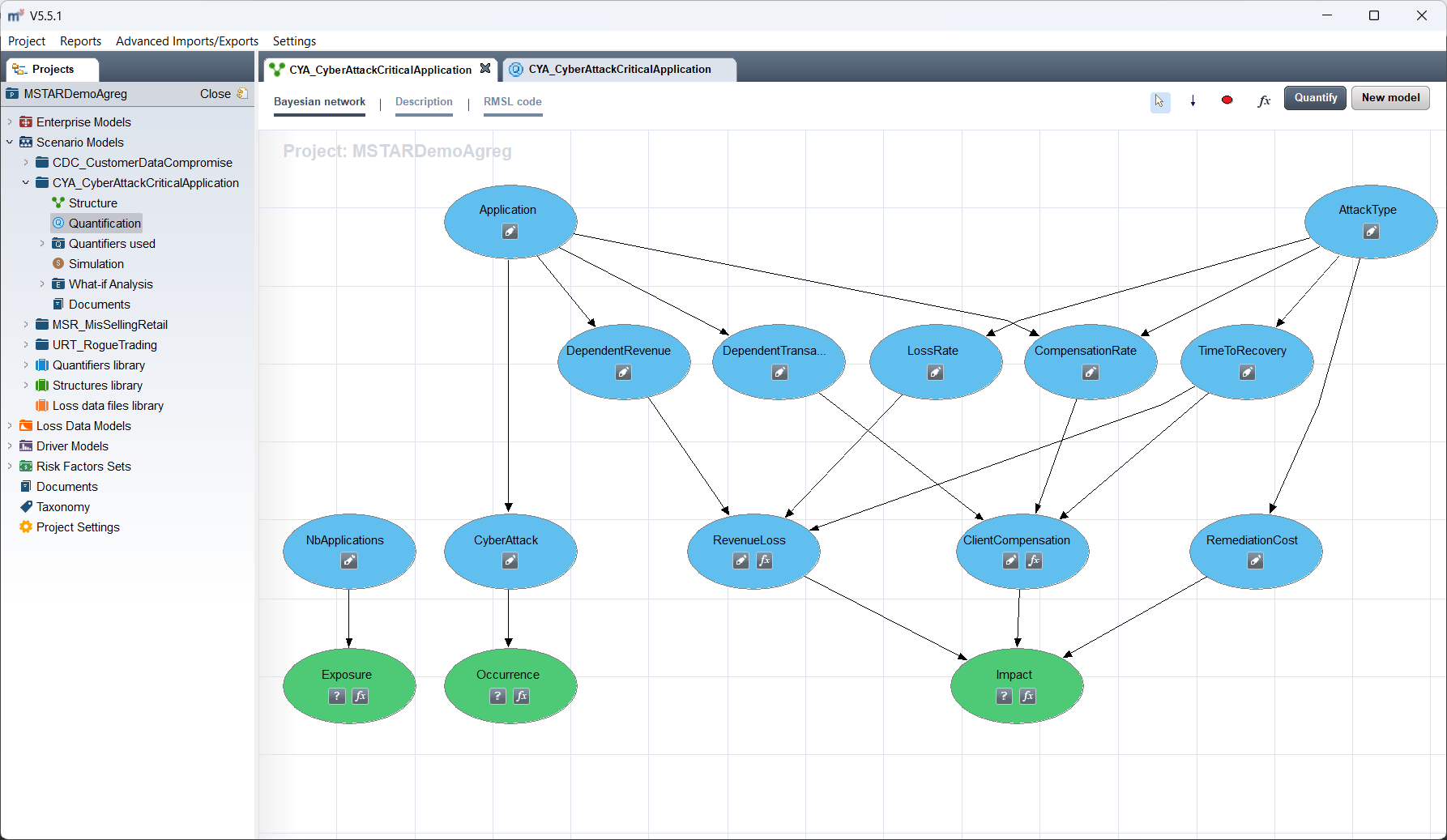

Define the model structure by setting up the causal relationships and the key drivers of Exposure, Occurrence, and Impact.

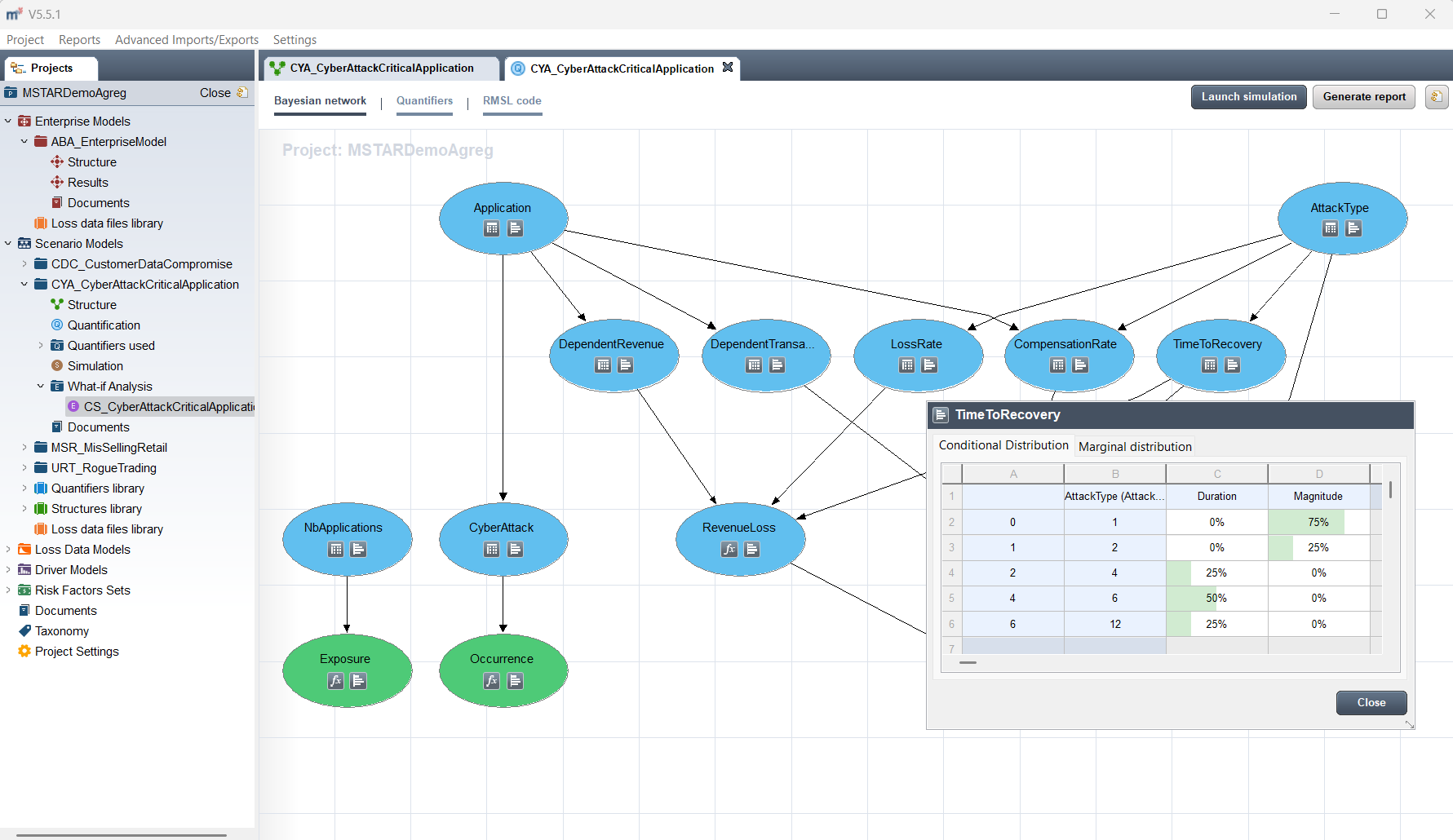

Attach quantifiers to each node: values, ranges, or distributions, based on expert judgment, internal data, or external sources.

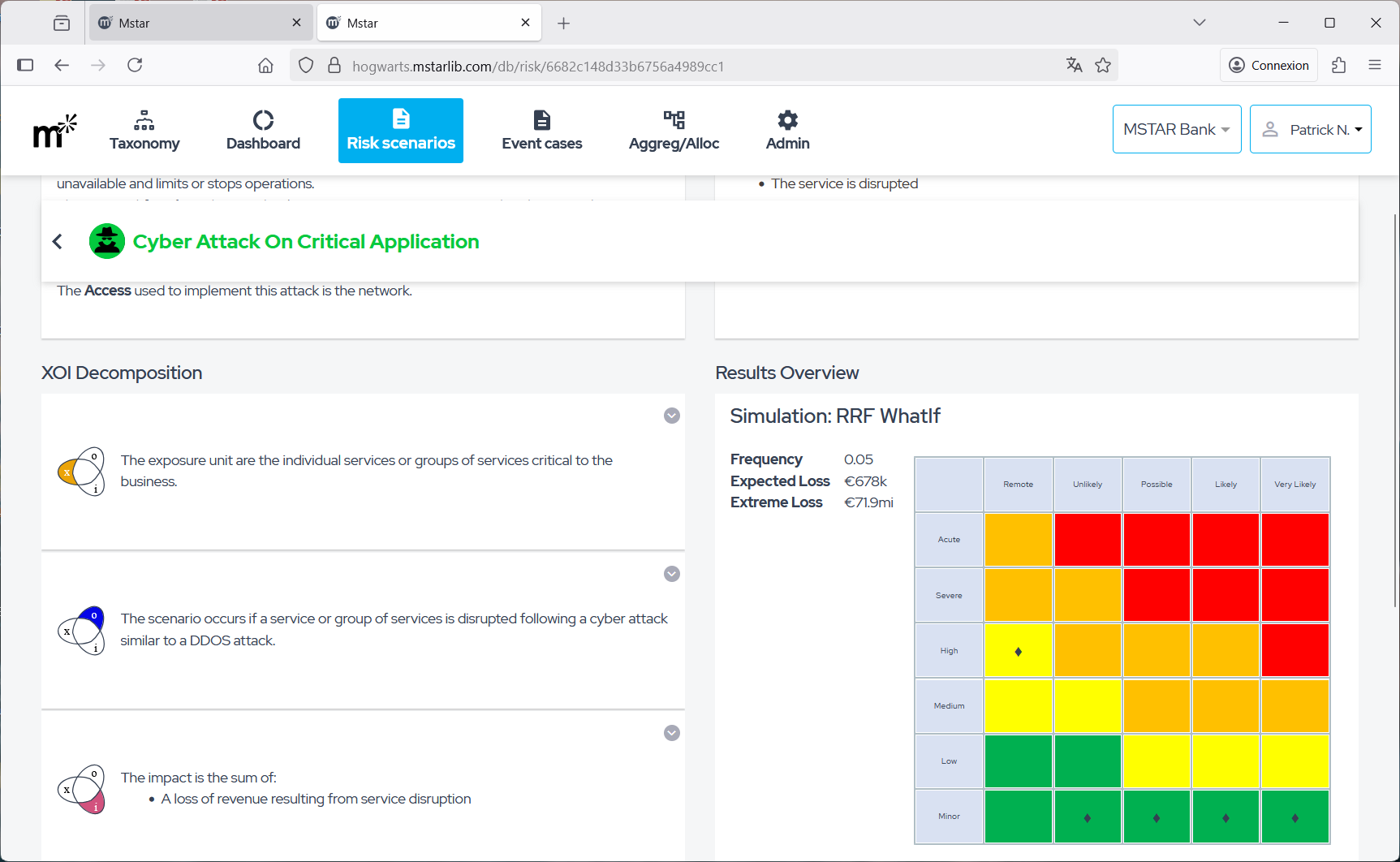

Run Monte Carlo simulations to explore a wide range of possible future situations and derive the distribution of potential losses.

Present results in a customizable risk grid that can directly support and facilitate the completion of a quantitative Risk and Control Assessment (RCA).

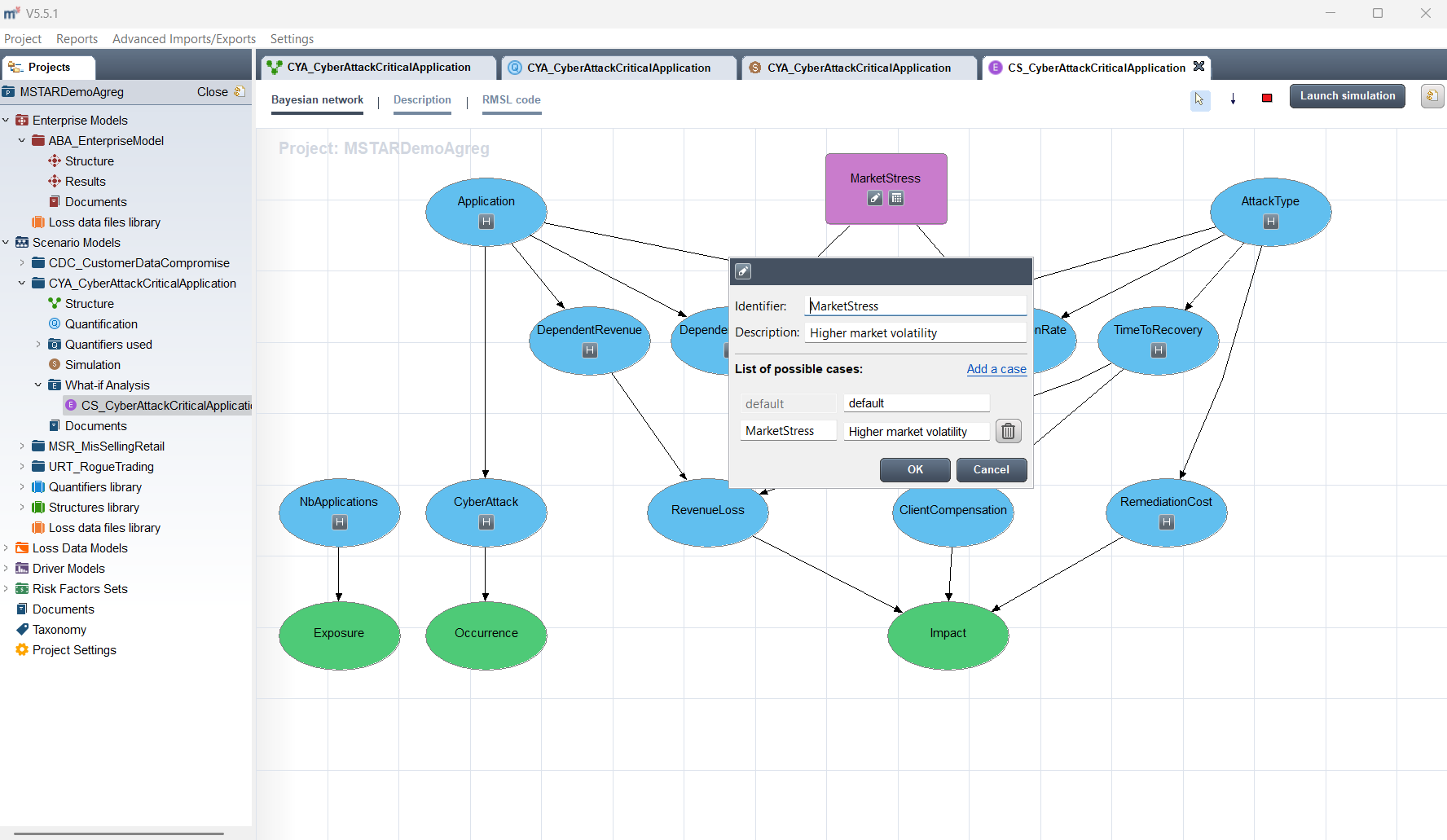

Set up what-if analyses to model external stresses, enhanced controls, or challenger expert assessments. These can affect one or multiple drivers.

Simulate scenarios under different assumptions from the what-if analysis to evaluate impacts at varying probability levels.

Assess dependencies between scenarios with an intuitive method that ensures the correlation matrix remains mathematically valid (positive semi-definite)

Visualize and edit the correlation matrix while maintaining mathematical consistency at all times

Run joint simulations using a copula on the defined dependency structure. Aggregation results highlight diversification effects across different probability levels.

MSTAR Desktop: Oprisk Scenario Design

MSTAR Desktop implements the XOI method for designing and quantifying your own risk scenarios, from

rogue trading to natural disasters by identifying exposure, assessing occurrence probabilities, and calculating impacts.

MSTAR Desktop can also generate simulation scripts

in Python, R, or Matlab for integration into external applications

MSTAR Platform: Oprisk

Scenario Library

The award winning MSTAR Platform (Risk.net 2020) offers a free curated news feed linking real-world events to our risk scenarios.

Subscribers unlock a comprehensive library of 40+ operational risk scenarios across Conduct, Cyber, Errors, and more.

With the Enterprise platform (on-premise), everything can be fully customized to your organization’s needs.

...

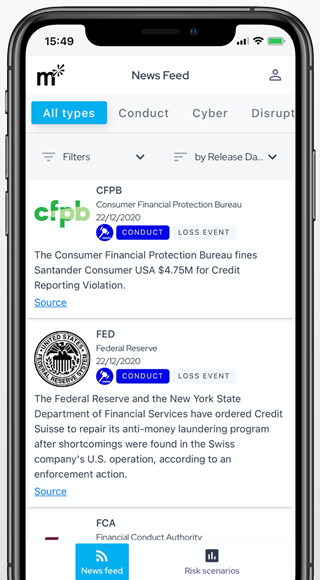

Access curated operational risk news, each linked to one of our 40+ scenarios (free).

Visualize your operational risk dashboard by category, with expected and extreme loss values (on-premise platform).

Explore the design and quantification of 40+ scenarios across Conduct, Cyber, Errors, Disruption, and more (consultation platform).

Browse detailed scenario designs and quantifiers, updated quarterly (consultation platform).

Customize scenarios online with your own assumptions and data for tailored risk analysis (on-premise platform).

MSTAR App: News & Scenarios on iOS & Android

Newsfeed

Stay updated on operational risk events globally.

Scenario Library

Access 40 scenarios of all risk types: Conduct, ESG, Cyber, Fraud, Error, Disruption, and Legal.